Disclosure: always be sure to consult your attorney with any investment decisions, this series is for educational purposes only.

LookFar Ventures14 October 2016

Demystifying Startup Finance Part IV: Understanding Dilution

This is Part 4 in our Demystifying Startup Finance series. Follow the links to read part 1, part 2, part 3, and part 5.

Let’s talk dilution – financial, not chemical. In finance, dilution is the decrease in percent equity held by investors’ shares by the addition of a new investment.

For each round of funding a startup takes on, the available number of shares increases. Therefore, while the number of shares held by a given person or party remains the same, the total number of shares outstanding increases, which shifts the percentage of equity held.

The assumed monetary value of shares held by any one investor is the number of shares held multiplied by the most recent valuation’s price-per-share. So, provided all rounds are up rounds the value of the shares held will continue to increase.

Dilution and associated provisions on term sheets are essential for founders to understand as it significantly affects their potential payout in the event of an exit.

It’s a fairly simple concept, but I’ll be the first to admit that it’s not so easy to put into words. So let’s actually look at some numbers and examine a hypothetical startup’s cap table as they raise three rounds of funding without convertible notes, employee stock option plans (ESOP), etc. Pay particular attention to how each party’s percent equity changes throughout the process.

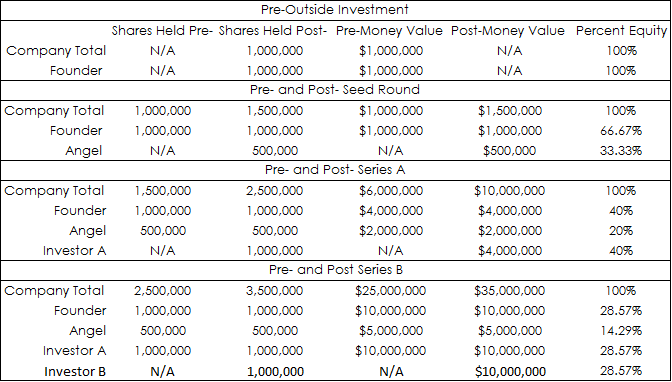

Our scenario starts with an entirely founder-held startup. The next step begins with an angel investor and the startup’s founder deciding on $1M as a pre-money valuation, with 1M shares outstanding. At this amount, the pre-money price-per-share is $1. This decision is portrayed in the “Pre-Outside Investment” section of the above table. This does not provide any information about the amount of self-funding the founder provided, but rather the amount that she and the angel agreed upon at valuation. Now, let’s walk through the rest of the cap table, starting with the seed round:

- The investor agrees to invest $500k at this time, they will receive 500k shares ($500k * $1 per share).

- Going into a Series A round, the company is appraised for $6M, this becomes the pre-money valuation of the company.

- At 1.5M shares outstanding, this brings the price-per-share up to $4 per share (6M/1.5M).

- The investor and founder agree on a $4M investment. At $4 per share, this entitles them to 1M shares, and 40% of the company effectively (1M/2.5M shares outstanding).

- As you can see, the immediate pre-money and post-money valuations by investor remain the same during a round. Only the percentage of equity held per owner and number of owners changes. This is because the value of each share changes between rounds, not when new money enters the bank.

- The post-money valuation of the company as a whole increases with number of shares outstanding/available.

- Number of shares held multiplied by pre-money price-per-share is the implied value from point of valuation until next investment made. Therefore, if number of shares held by a party is consistent, the value of that number of shares multiplied by the pre-money price-per-share will remain the same until there is a new pre-money valuation.

- During the company’s Series B, an investor and the founder agree to $25M pre-money. This raises the price-per-share to $10 a share (25M/2.5M shares outstanding). They also agree to a $10M raise. At the current price-per-share, this becomes 1M shares, and 28.57% stake in the company.

- Note here investor for series B receives the same amount of shares/equity as the investor from series A. The dramatic increase in pre-money valuation from seed to series B could be caused by noteable market validation, increase in revenue, or other positive signs about the future of the company. Forward progress increases the chances of success and decreases the risk of investing in the company. The investor from series A invested at a higher level of risk, and therefore (in absence of any combination of possible terms held by series B) will receive a higher reward if the two exit at the same time.

From this point, the company can continue to raise money and dilute the shares as it has been, or position itself for an exit. An exit can be an IPO (Initial Public Offering), an acquisition, or a liquidation in the event of company failure.

Dilution can be tricky to understand and will be different for each company depending on the terms agreed upon with each investor. Anti-dilution Clauses, requirement of ESOPs, and other terms can alter the dilution each founder experiences in each round. Mark Suster’s TechCrunch graphic provides a breakdown of dilution when taking ESOPs into consideration.

A major takeaway I’d like to leave you with: at the end of the day, the percent held by any given party is the amount of the capital outcome they have a claim to. However, depending on the terms held by herself and other investors, this number may be a far cry from the actual percentage of the final post-money valuation. Furthermore, these earnings or losses are subject to taxes based on the state in which the company or party is located and the type of exit that occurs.

Buyers of preferred stock have the ability to negotiate an anti-dilution provision to protect themselves in the event of a down round. Check out our next post about the options available to founders and investors.

The cap table above is unlikely to occur as is, because it lacks consideration for anti-dilution and liquidation preferences. To learn more about term sheet provisions that can affect cap tables, stay tuned for future posts.

Written by

How to Build Your Magic Machine: A primer on technical development for Startup Founders

How to Build Your Magic Machine: A primer on technical development for Startup Founders

Net Neutrality in the Southeast: Why Emerging Hubs Should Fight for Title II

Net Neutrality in the Southeast: Why Emerging Hubs Should Fight for Title II

Copyright © 2025 LookFar Labs. All rights reserved. Privacy Policy